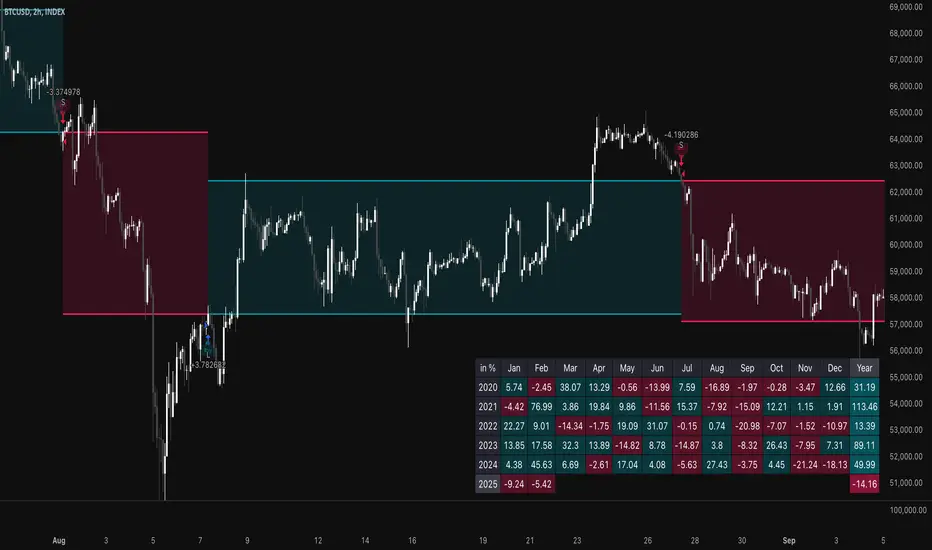

TSI Long/Short for BTC 2HThe TSI Long/Short for BTC 2H strategy is an advanced trend-following system designed specifically for trading Bitcoin (BTC) on a 2-hour timeframe. It leverages the True Strength Index (TSI) to identify momentum shifts and executes both long and short trades in response to dynamic market conditions.

Unlike traditional moving average-based strategies, this script uses a double-smoothed momentum calculation, enhancing signal accuracy and reducing noise. It incorporates automated position sizing, customizable leverage, and real-time performance tracking, ensuring a structured and adaptable trading approach.

🔹 What Makes This Strategy Unique?

Unlike simple crossover strategies or generic trend-following approaches, this system utilizes a customized True Strength Index (TSI) methodology that dynamically adjusts to market conditions.

🔸 True Strength Index (TSI) Filtering – The script refines the TSI by applying double exponential smoothing, filtering out weak signals and capturing high-confidence momentum shifts.

🔸 Adaptive Entry & Exit Logic – Instead of fixed thresholds, it compares the TSI value against a dynamically determined high/low range from the past 100 bars to confirm trade signals.

🔸 Leverage & Risk Optimization – Position sizing is dynamically adjusted based on account equity and leverage settings, ensuring controlled risk exposure.

🔸 Performance Monitoring System – A built-in performance tracking table allows traders to evaluate monthly and yearly results directly on the chart.

📊 Core Strategy Components

1️⃣ Momentum-Based Trade Execution

The strategy generates long and short trade signals based on the following conditions:

✅ Long Entry Condition – A buy signal is triggered when the TSI crosses above its 100-bar highest value (previously set), confirming bullish momentum.

✅ Short Entry Condition – A sell signal is generated when the TSI crosses below its 100-bar lowest value (previously set), indicating bearish pressure.

Each trade execution is fully automated, reducing emotional decision-making and improving trading discipline.

2️⃣ Position Sizing & Leverage Control

Risk management is a key focus of this strategy:

🔹 Dynamic Position Sizing – The script calculates position size based on:

Account Equity – Ensuring trade sizes adjust dynamically with capital fluctuations.

Leverage Multiplier – Allows traders to customize risk exposure via an adjustable leverage setting.

🔹 No Fixed Stop-Loss – The strategy relies on reversals to exit trades, meaning each position is closed when the opposite signal appears.

This design ensures maximum capital efficiency while adapting to market conditions in real time.

3️⃣ Performance Visualization & Tracking

Understanding historical performance is crucial for refining strategies. The script includes:

📌 Real-Time Trade Markers – Buy and sell signals are visually displayed on the chart for easy reference.

📌 Performance Metrics Table – Tracks monthly and yearly returns in percentage form, helping traders assess profitability over time.

📌 Trade History Visualization – Completed trades are displayed with color-coded boxes (green for long trades, red for short trades), visually representing profit/loss dynamics.

📢 Why Use This Strategy?

✔ Advanced Momentum Detection – Uses a double-smoothed TSI for more accurate trend signals.

✔ Fully Automated Trading – Removes emotional bias and enforces discipline.

✔ Customizable Risk Management – Adjust leverage and position sizing to suit your risk profile.

✔ Comprehensive Performance Tracking – Integrated reporting system provides clear insights into past trades.

This strategy is ideal for Bitcoin traders looking for a structured, high-probability system that adapts to both bullish and bearish trends on the 2-hour timeframe.

📌 How to Use: Simply add the script to your 2H BTC chart, configure your leverage settings, and let the system handle trade execution and tracking! 🚀

"the script" için komut dosyalarını ara

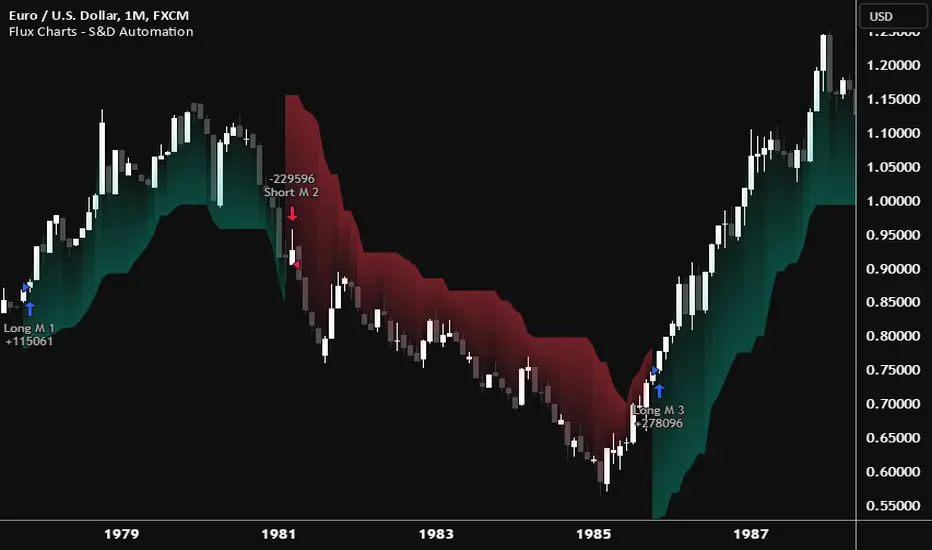

Flux Charts - S&D Automation💎 GENERAL OVERVIEW

The MTF Supply & Demand Zones (S&D) Automation is a powerful and versatile tool designed to help traders rigorously test their trading strategies against historical market data. With various advanced settings, traders can fine-tune their strategies, assess performance, and identify key improvements before deploying in live trading environments. This tool offers a wide range of configurable settings, explained within this write-up.

Features of the new S&D Automation:

Step By Step : Configure your strategy step by step, which will allow you to have OR & AND logic in your strategies.

Highly Configurable : Offers multiple parameters for fine-tuning trade entry and exit conditions.

Multi-Timeframe Analysis : Allows traders to analyze multiple timeframes simultaneously for enhanced accuracy.

Provides advanced stop-loss, take-profit, and break-even settings.

Incorporates Supply & Demand Zone conditions, with settings like Sensitivity, Zone Invalidation, Minimum Zone Width & Minimum Zone Length settings for refined strategy execution.

🚩 UNIQUENESS

The S&D Automation stands out from conventional backtesting tools due to its unparalleled flexibility, precision, and advanced trading logic integration. Key factors that make it unique include:

✅ Comprehensive Strategy Customization – Unlike traditional backtesters that offer basic entry and exit conditions, S&D Automation provides a highly detailed parameter set, allowing traders to fine-tune their strategies with precision.

✅ Multi-Timeframe Supply & Demand Zones – This is the first-ever tool that allows traders to backtest Supply & Demand zones on multiple timeframes.

✅ Customizable Take-Profit Conditions – Offers various methods to set take-profit exits, including using core features from Supply & Demand Zones, and fixed exits like ATR, % change or price change, enabling traders to tailor their exit strategies to specific market behaviors.

✅ Customizable Stop-Loss Conditions – Provides several ways to set up stop losses, including using concepts from Supply & Demand Zones and trailing stops or fixed exits like ATR, % change or price change, allowing for dynamic risk management tailored to individual strategies.

✅ Integration of External Indicators – Allows the inclusion of other indicators or data sources from TradingView for creating strategy conditions, enabling traders to enhance their strategies with additional insights and data points.

By integrating these advanced features, S&D Automation ensures that traders can rigorously test and optimize their strategies with great accuracy and efficiency.

📌 HOW DOES IT WORK ?

The first setting you will want to set it the pyramiding setting. This setting controls the number of simultaneous trades in the same direction allowed in the strategy. For example, if you set it to 1, only one trade can be active in any time, and the second trade will not be entered unless the first one is exited. If it is set to 2, the script will handle both of them at the same time. Note that you should enter the same value to this pyramiding setting, and the pyramiding setting in the "Properties" tab of the script for this to work.

You can enable and set a backtesting window that will limit the entries to between the start date & end date.

Then, you can enter your desired settings for Supply & Demand Zones. You can also enable and set up to 3 timeframes, which you can use later on when customizing your strategies enter / exit conditions.

Entry Conditions

From the "Long Conditions" or the "Short Conditions" groups, you can set your position entry conditions. For settings like "initial capital" or "order size", you can open the "Properties" tab, where these are handled.

The S&D Automation can use the following conditions for entry conditions :

1. Demand Zone

Detection: Triggered when a Demand Zone forms or is detected

Retest: Triggered when price retests a Demand Zone. A retest is confirmed when a candle enters a Demand Zone and closes outside of it.

2nd Retest: Triggered when price retests a Demand Zone for the second time. A retest is confirmed when a candle enters a Demand Zone and closes outside of it.

3rd Retest: Triggered when price retests a Demand Zone for the third time. A retest is confirmed when a candle enters a Demand Zone and closes outside of it.

Retracement: Triggered when price touches a Demand Zone

Break: Triggered when a Demand Zone is invalidated by candle close or wick, depending on the user's input.

2. Supply Zone

Detection: Triggered when a Supply Zone forms or is detected

Retest: Triggered when price retests a Supply Zone. A retest is confirmed when a candle enters a Supply Zone and closes outside of it.

2nd Retest: Triggered when price retests a Supply Zone for the second time. A retest is confirmed when a candle enters a Supply Zone and closes outside of it.

3rd Retest: Triggered when price retests a Supply Zone for the third time. A retest is confirmed when a candle enters a Supply Zone and closes outside of it.

Retracement: Triggered when price touches a Supply Zone

Break: Triggered when a Supply Zone is invalidated by candle close or wick, depending on the user's input.

3. Any Zone

Detection: Triggered when any Supply or Demand Zone forms or is detected

Retest: Triggered when price retests any Supply or Demand Zone. A retest is confirmed when a candle enters any Supply or Demand Zone and closes outside of it.

2nd Retest: Triggered when price retests any Supply or Demand Zone for the second time. A retest is confirmed when a candle enters any Supply or Demand Zone and closes outside of it.

3rd Retest: Triggered when price retests any Supply or Demand Zone for the third time. A retest is confirmed when a candle enters any Supply or Demand Zone and closes outside of it.

Retracement: Triggered when price touches any Supply or Demand Zone

Break: Triggered when any Supply or Demand Zone is invalidated by candle close or wick, depending on the user's input.

🕒 TIMEFRAME CONDITIONS

The S&D Automation supports Multi-Timeframe (MTF) features, just like the Supply & Demand indicator. When setting an entry condition, you can also choose the timeframe.

To set up MTF conditions, navigate to the 'Timeframes' section in the settings, select your desired timeframes, and enable them. You can choose up to three timeframes.

Once you've selected your timeframes, you can use them in your strategy. When setting long and short entry/exit conditions, you can choose from Timeframe 1, Timeframe 2, or Timeframe 3.

External Conditions

Users can use external indicators on the chart to set entry conditions.

The second dropdown in the external condition settings allows you to choose a conditional operator to compare external outputs. Available options include:

Less Than or Equal To: <=

Less Than: <

Equal To: =

Greater Than: >

Greater Than or Equal To: >=

The position entry conditions work like this ;

Each side has 5 S&D Zone conditions and 1 Source condition. Each condition can be enabled or disabled using the checkbox on the left side of them.

The next selection is the alert type, which you can select between "Detection", "Retest", "Retracement" or "Break".

You can select which timeframe this condition should work on from Timeframe 1, 2, or 3. If you select "Any Timeframe", the condition will work for all timeframes.

Lastly select the step of this condition from 1 to 6.

The Source Condition

The last condition on each side is a source condition that is different from the others. Using this condition, you can create your own logic using other indicators' outputs on your chart. For example, suppose that you have an EMA indicator in your chart. You can have the source condition to something like "EMA > high".

The Step System

Each condition has a step number, and conditions are in topological order based on them.

The conditions are executed step by step. This means the condition with step 2 cannot be executed before the condition with step 1 is executed.

Conditions with the same step numbers have "OR" logic. This means that if you have 2 conditions with step 3, the condition with step 4 can trigger after only one of the step 3 conditions is executed.

➕ OTHER ENTRY FEATURES

The S&D Automation allows traders to choose when to execute trades and when not to execute trades.

1. Only Take Trades

This setting lets users specify the time period when their strategy can open or execute trades.

2. Don't Take Trades

This setting lets users specify time periods when their strategy can't open or execute trades.

↩️ EXIT CONDITIONS

1. Exit on Opposite Signal

When enabled, a long position will close when short entry conditions are met, and a short position will close when long entry conditions are met.

2. Exit on Session End

When enabled, positions will be closed at the end of the trading session.

📈 TAKE PROFIT CONDITIONS

There are several methods available for setting take profit exits and conditions.

1. Entry Condition TP

Users can use entry conditions as triggers for take-profit exits. This setting can be found under the long and short exit conditions.

2. Fixed TP

Users can set a fixed TP for exits. This setting can be found under the long and short exit conditions. Users can choose between the following:

Price: This method triggers a TP exit when price reaches a specified level. For example, if you set the Price TP to 10 and buy NASDAQ:TSLA at $190, the trade will automatically exit when the price reaches $200 ($190 + $10).

Ticks: This method triggers a TP exit when price moves a specified number of ticks.

Percentage (%): This method triggers a TP exit when price moves a specified percentage.

ATR: This method triggers a TP exit based on a specified multiple of the Average True Range (ATR).

📉 STOP LOSS CONDITIONS

There are several methods available for setting stop-loss exits and conditions.

1. Entry Condition SL

Users can use entry conditions as triggers for stop-loss exits. This setting can be found under the long and short exit conditions.

2. Fixed SL

Users can set a fixed SL for exits. This setting can be found under the long and short exit conditions. Users can choose between the following:

Price: This method triggers a SL exit when price reaches a specified level. For example, if you set the Price SL to 10 and buy NASDAQ:TSLA at $200, the trade will automatically exit when the price reaches $190 ($200 - $10).

Ticks: This method triggers a SL exit when price moves a specified number of ticks.

Percentage (%): This method triggers a SL exit when price moves a specified percentage.

ATR: This method triggers a SL exit based on a specified multiple of the Average True Range (ATR).

3. Trailing Stop

An explanation & example for the trailing stop feature is present on the write-up within the next section.

Exit conditions have the same logic of constructing conditions like the entry ones. You can construct a Take-Profit Condition & a Stop-Loss Condition. Note that the Take-Profit condition will only work if the position is in profit, regardless of if it's triggered or not. The same applies for the Stop-Loss condition, meaning that it will only work if the position is in loss.

You can also set a Fixed TP & Fixed SL based on the price movement after the position is entered. You have options like "Price", "Ticks", "%", or "Average True Range". For example, you can set a Fixed TP like "5%", and the position will be entered once it moves 5% up in a long position.

Trailing Stop

For the Fixed SL, you also have a "Trailing" stop option, for which you can set its activation level as well. The Trailing stop activation level and its value are expressed in ticks. Check this scenario for an example :

We have a ticker with a tick value of $1. Our Trailing Stop is set to 10 ticks, and the activation level is set to 30 ticks.

We buy 1 contract when the price is $100.

When the price becomes $110, we are in $10 (10 ticks) profit and the trailing stop is now activated.

The current price our stop's on is $110 - $30 (30 ticks), which is the level of $80.

The trailing stop will only move if the price moves up the highest high the price has been after we entered the position.

Let's suppose that price moves up $40 right after our trailing stop is activated. The price will now be $150, and our trailing stop will sit on $150 - $30 (30 ticks) = $120.

If the price is down the $120 level, our stop loss will be triggered.

There is also a "Hard SL" option designed for a backup stop-loss when trailing stops are enabled. You can enable & set this option and if the price goes down before our trailing stop even activates, the position will be exited.

You can also move stop-loss to the break-even (entry price of the position) after a certain profit is achieved using the last setting of the exit conditions. Note that for this to work, you must have a Fixed SL set-up.

➕ OTHER EXIT FEATURES

1. Move Stop Loss to Breakeven

This setting allows the strategy to automatically move the SL to Breakeven (BE) when the position is in profit by a certain amount. Users can choose between the following:

Price: This method moves the SL to BE when price reaches a specified level.

Ticks: This method moves the SL to BE when price moves a specified number of ticks.

Percentage (%): This method moves the SL to BE when price moves a specified percentage.

ATR: This method moves the SL to BE when price moves a specified multiple of the Average True Range (ATR).

Example Entry Scenario

To give an example , check this scenario; out conditions are :

LONG CONDITIONS

Demand Zone Detection, Step 1

Supply Zone Retest, Step 2

Demand Zone Break, Step 2

open > close, Step 3

First, the strategy needs to detect a Demand Zone Detection in order to start working.

After it's detected, now it's looking for either a Supply Zone Retest, or a Demand Zone Break to proceed to the next step, the reason for this is that they both have the same step number.

After one of them is detected, the strategy will consistently check candlesticks for the condition open > close. If a bullish candlestick occurs, a long position will be entered.

⏰ ALERTS

This indicator uses TradingView's strategy alert system. All entries and exits will be sent as an alert if configured. It's possible to further customize these alerts to your liking. For more information check TradingView's strategy alert customization page : www.tradingview.com

⚙️ SETTINGS

1. Backtesting Settings

Pyramiding: Controls the number of simultaneous trades allowed in the strategy. This setting must have the same value that is entered on the script's properties tab on the settings pane.

Enable Custom Backtesting Period: Restricts backtesting to a specific date range.

Start & End Time Configuration: Define precise start and end dates for historical analysis.

2. General Configuration

Detection Method: There are two detection methods you can choose from for identifying Supply & Demand Zones. Both methods aim to identify key areas where price is likely to react, but they do so using different approaches. Traders can choose the method that aligns with their trading style and time horizon.

Sensitivity: The Sensitivity setting allows traders to adjust how aggressively the script identifies supply and demand zones when using the Momentum Detection Method. This setting directly impacts the threshold for detecting zones when using the momentum detection method.

Zone Invalidation: The Zone Invalidation setting determines how supply and demand zones are invalidated.

Wick -> A zone is invalidated if a candle’s wick goes below a demand zone or above a supply zone.

Close -> A zone is invalidated if a candle closes below a demand zone or above a supply zone.

Zone Visibility Range: The Zone Visibility Range setting controls how far from the current price supply and demand zones are displayed on the chart. It helps traders focus on relevant zones while avoiding clutter from distant or less impactful areas.

Minimum Zone Width: The Minimum Zone Width setting defines the smallest size a supply or demand zone must have to be displayed on the chart. It uses the Average True Range (ATR) as a reference to ensure zones are proportionate to current market volatility.

Minimum Zone Length: The Minimum Zone Length setting determines the minimum number of bars a supply or demand zone must span to be displayed on the chart. This setting helps filter out short-lived or insignificant zones, ensuring only meaningful areas of supply or demand are highlighted.

3. Multi-Timeframe Analysis

Enable Up to Three Timeframes: Select and analyze trades across multiple timeframes.

4. Entry Conditions for Long & Short Trades

Multiple Conditions (1-6): Configure up to six independent conditions per trade direction.

Condition Types: Options include Detection, Retest, 2nd Retest, 3rd Retest, Retracement, and Break.

Timeframe Specification: Choose between "Any Timeframe", "Timeframe 1", "Timeframe 2", or "Timeframe 3".

Trade Execution Filters: Restrict trades within specific trading sessions.

5. Exit Conditions for Long & Short Trades

Exit on Opposite Signal: Automatically exit trades upon opposite trade conditions.

Exit on Session End: Closes all positions at the end of the trading session.

Multiple Take-Profit (TP) and Stop-Loss (SL) Configurations:

TP/SL based on % move, ATR, Ticks, or Fixed Price.

Hard SL option for additional risk control.

Move SL to BE (Break Even) after a certain profit threshold.

Moving Average Crossover StrategyCertainly! Below is an example of a professional trading strategy implemented in Pine Script for TradingView. This strategy is a simple moving average crossover strategy, which is a common approach used by many traders. It uses two moving averages (a short-term and a long-term) to generate buy and sell signals.

Input Parameters:

shortLength: The length of the short-term moving average.

longLength: The length of the long-term moving average.

Moving Averages:

shortMA: The short-term simple moving average (SMA).

longMA: The long-term simple moving average (SMA).

Conditions:

longCondition: A buy signal is generated when the short-term MA crosses above the long-term MA.

shortCondition: A sell signal is generated when the short-term MA crosses below the long-term MA.

Trade Execution:

The strategy enters a long position when the longCondition is met.

The strategy enters a short position when the shortCondition is met.

Plotting:

The moving averages are plotted on the chart.

Buy and sell signals are plotted as labels on the chart.

How to Use:

Copy the script into TradingView's Pine Script editor.

Adjust the shortLength and longLength parameters to fit your trading style.

Add the script to your chart and apply it to your desired timeframe.

Backtest the strategy to see how it performs on historical data.

This is a basic example, and professional traders often enhance such strategies with additional filters, risk management rules, and other indicators to improve performance.

Advanced Multi-Timeframe Trading System (Risk Managed)Description:

This strategy is an original approach that combines two main analytical components to identify potential trade opportunities while simulating realistic trading conditions:

1. Market Trend Analysis via an Approximate Hurst Exponent

• What It Does:

The strategy computes a rough measure of market trending using an approximate Hurst exponent. A value above 0.5 suggests persistent, trending behavior, while a value below 0.5 indicates a tendency toward mean-reversion.

• How It’s Used:

The Hurst exponent is calculated on both the chart’s current timeframe and a higher timeframe (default: Daily) to capture both local and broader market dynamics.

2. Fibonacci Retracement Levels

• What It Does:

Using daily high and low data from a selected timeframe (default: Daily), the script computes key Fibonacci retracement levels.

• How It’s Used:

• The 61.8% level (Golden Ratio) serves as a key threshold:

• A long entry is signaled when the price crosses above this level if the daily Hurst exponent confirms a trending market.

• The 38.2% level is used to identify short-entry opportunities when the price crosses below it and the daily Hurst indicates non-trending conditions.

Signal Logic:

• Long Entry:

When the price crosses above the 61.8% Fibonacci level (Golden Ratio) and the daily Hurst exponent is greater than 0.5, suggesting a trending market.

• Short Entry:

When the price crosses below the 38.2% Fibonacci level and the daily Hurst exponent is less than 0.5, indicating a less trending or potentially reversing market.

Risk Management & Trade Execution:

• Stop-Loss:

Each trade is risk-managed with a stop-loss set at 2% below (for longs) or above (for shorts) the entry price. This ensures that no single trade risks more than a small, sustainable portion of the account.

• Take Profit:

A take profit order targets a risk-reward ratio of 1:2 (i.e., the target profit is twice the amount risked).

• Position Sizing:

Trades are executed with a fixed position size equal to 10% of account equity.

• Trade Frequency Limits:

• Daily Limit: A maximum of 5 trades per day

• Overall Limit: No more than 510 trades during the backtesting period (e.g., since 2019)

These limits are imposed to simulate realistic trading frequency and to avoid overtrading in backtest results.

Backtesting Parameters:

• Initial Capital: $10,000

• Commission: 0.1% per trade

• Slippage: 1 tick per bar

These settings aim to reflect the conditions faced by the average trader and help ensure that the backtesting results are realistic and not misleading.

Chart Overlays & Visual Aids:

• Fibonacci Levels:

The key Fibonacci retracement levels are plotted on the chart, and the zone between the 61.8% and 38.2% levels is highlighted to show a key retracement area.

• Market Trend Background:

The chart background is tinted green when the daily Hurst exponent indicates a trending market (value > 0.5) and red otherwise.

• Information Table:

An on-chart table displays key parameters such as the current Hurst exponent, daily Hurst value, the number of trades executed today, and the global trade count.

Disclaimer:

Past performance is not indicative of future results. This strategy is experimental and provided solely for educational purposes. It is essential that you backtest and paper trade using your own settings before considering any live deployment. The Hurst exponent calculation is an approximation and should be interpreted as a rough gauge of market behavior. Adjust the parameters and risk management settings according to your personal risk tolerance and market conditions.

Additional Notes:

• Originality & Usefulness:

This script is an original mashup that combines trend analysis with Fibonacci retracement methods. The description above explains how these components work together to provide trading signals.

• Realistic Results:

The strategy uses realistic account sizes, commission rates, slippage, and risk management rules to generate backtesting results that are representative of real-world trading.

• Educational Purpose:

This script is intended to support the TradingView community by offering insights into combining multiple analysis techniques in one strategy. It is not a “get-rich-quick” system but rather an educational tool to help traders understand risk management and trade signal logic.

By using this script, you acknowledge that trading involves risk and that you are responsible for testing and adjusting the strategy to fit your own trading environment. This publication is fully open source, and any modifications should include proper attribution if significant portions of the code are reused.

Dow Theory Swing Trading-DexterThis Pine Script strategy that implements a basic price action-based trading system inspired by Dow Theory, focusing on swing highs and swing lows. This strategy will generate buy and sell signals based on the formation of higher highs (HH) and higher lows (HL) for an uptrend, and lower highs (LH) and lower lows (LL) for a downtrend.

Swing Highs and Swing Lows:

The script identifies swing highs and swing lows using the ta.highest and ta.lowest functions over a specified lookback period.

A swing high is identified when the high of the current bar is the highest high over the lookback period.

A swing low is identified when the low of the current bar is the lowest low over the lookback period.

Trend Detection:

An uptrend is detected when the current low is higher than the last identified swing low.

A downtrend is detected when the current high is lower than the last identified swing high.

Buy and Sell Signals:

A buy signal is generated when the price closes above the last swing high during an uptrend.

A sell signal is generated when the price closes below the last swing low during a downtrend.

Plotting:

Swing highs and swing lows are plotted on the chart using plotshape.

Buy and sell signals are also plotted on the chart for visual reference.

How to Use:

Copy and paste the script into the Pine Script editor in TradingView.

Adjust the lookback period as needed to suit your trading style and timeframe.

Apply the script to your chart and it will generate buy and sell signals based on the price action.

NOTE: Please uncheck the all the unwanted symbol from chart for clear view .

Forex Hammer and Hanging Man StrategyThe strategy is based on two key candlestick chart patterns: Hammer and Hanging Man. These chart patterns are widely used in technical analysis to identify potential reversal points in the market. Their relevance in the Forex market, known for its high liquidity and volatile price movements, is particularly pronounced. Both patterns provide insights into market sentiment and trader psychology, which are critical in currency trading, where short-term volatility plays a significant role.

1. Hammer:

• Typically occurs after a downtrend.

• Signals a potential trend reversal to the upside.

• A Hammer has:

• A small body (close and open are close to each other).

• A long lower shadow, at least twice as long as the body.

• No or a very short upper shadow.

2. Hanging Man:

• Typically occurs after an uptrend.

• Signals a potential reversal to the downside.

• A Hanging Man has:

• A small body, similar to the Hammer.

• A long lower shadow, at least twice as long as the body.

• A small or no upper shadow.

These patterns are a manifestation of market psychology, specifically the tug-of-war between buyers and sellers. The Hammer reflects a situation where sellers tried to push the price down but were overpowered by buyers, while the Hanging Man shows that buyers failed to maintain the upward movement, and sellers could take control.

Relevance of Chart Patterns in Forex

In the Forex market, chart patterns are vital tools because they offer insights into price action and market sentiment. Since Forex trading often involves large volumes of trades, chart patterns like the Hammer and Hanging Man are important for recognizing potential shifts in market momentum. These patterns are a part of technical analysis, which aims to forecast future price movements based on historical data, relying on the psychology of market participants.

Scientific Literature on the Relevance of Candlestick Patterns

1. Behavioral Finance and Candlestick Patterns:

Research on behavioral finance supports the idea that candlestick patterns, such as the Hammer and Hanging Man, are relevant because they reflect shifts in trader psychology and sentiment. According to Lo, Mamaysky, and Wang (2000), patterns like these could be seen as representations of collective investor behavior, influenced by overreaction, optimism, or pessimism, and can often signal reversals in market trends.

2. Statistical Validation of Chart Patterns:

Studies by Brock, Lakonishok, and LeBaron (1992) explored the profitability of technical analysis strategies, including candlestick patterns, and found evidence that certain patterns, such as the Hammer, can have predictive value in financial markets. While their study primarily focused on stock markets, their findings are generally applicable to the Forex market as well.

3. Market Efficiency and Candlestick Patterns:

The efficient market hypothesis (EMH) posits that all available information is reflected in asset prices, but some studies suggest that markets may not always be perfectly efficient, allowing for profitable exploitation of certain chart patterns. For instance, Jegadeesh and Titman (1993) found that momentum strategies, which often rely on price patterns and trends, could generate significant returns, suggesting that patterns like the Hammer or Hanging Man may provide a slight edge, particularly in short-term Forex trading.

Testing the Strategy in Forex Using the Provided Script

The provided script allows traders to test and evaluate the Hammer and Hanging Man patterns in Forex trading by entering positions when these patterns appear and holding the position for a specified number of periods. This strategy can be tested to assess its performance across different currency pairs and timeframes.

1. Testing on Different Timeframes:

• The effectiveness of candlestick patterns can vary across different timeframes, as market dynamics change with the level of detail in each timeframe. Shorter timeframes may provide more frequent signals, but with higher noise, while longer timeframes may produce more reliable signals, but with fewer opportunities. This multi-timeframe analysis could be an area to explore to enhance the strategy’s robustness.

2. Exit Strategies:

• The script incorporates an exit strategy where positions are closed after holding them for a specified number of periods. This is useful for testing how long the reversal patterns typically take to play out and when the optimal exit occurs for maximum profitability. It can also help to adjust the exit logic based on real-time market behavior.

Conclusion

The Hammer and Hanging Man patterns are widely recognized in technical analysis as potential reversal signals, and their application in Forex trading is valuable due to the market’s high volatility and liquidity. This strategy leverages these candlestick patterns to enter and exit trades based on shifts in market sentiment and psychology. Testing and optimization, as offered by the script, can help refine the strategy and improve its effectiveness.

For further refinement, it could be valuable to consider combining candlestick patterns with other technical indicators or using multi-timeframe analysis to confirm patterns and increase the probability of successful trades.

References:

• Lo, A. W., Mamaysky, H., & Wang, J. (2000). Foundations of Technical Analysis: Computational Algorithms, Statistical Inference, and Empirical Implementation. The Journal of Finance, 55(4), 1705-1770.

• Brock, W., Lakonishok, J., & LeBaron, B. (1992). Simple Technical Trading Rules and the Stochastic Properties of Stock Returns. The Journal of Finance, 47(5), 1731-1764.

• Jegadeesh, N., & Titman, S. (1993). Returns to Buying Winners and Selling Losers: Implications for Stock Market Efficiency. The Journal of Finance, 48(1), 65-91.

This provides a theoretical basis for the use of candlestick patterns in trading, supported by academic literature and research on market psychology and efficiency.

Engulfing Candlestick StrategyEver wondered whether the Bullish or Bearish Engulfing pattern works or has statistical significance? This script is for you. It works across all markets and timeframes.

The Engulfing Candlestick Pattern is a widely used technical analysis pattern that traders use to predict potential price reversals. It consists of two candles: a small candle followed by a larger one that "engulfs" the previous candle. This pattern is considered bullish when it occurs in a downtrend (bullish engulfing) and bearish when it occurs in an uptrend (bearish engulfing).

Statistical Significance of the Engulfing Pattern:

While many traders rely on candlestick patterns for making decisions, research on the statistical significance of these patterns has produced mixed results. A study by Dimitrios K. Koutoupis and K. M. Koutoupis (2014), titled "Testing the Effectiveness of Candlestick Chart Patterns in Forex Markets," indicates that candlestick patterns, including the engulfing pattern, can provide some predictive power, but their success largely depends on the market conditions and timeframe used. The researchers concluded that while some candlestick patterns can be useful, traders must combine them with other indicators or market knowledge to improve their predictive accuracy.

Another study by Brock, Lakonishok, and LeBaron (1992), "Simple Technical Trading Rules and the Stochastic Properties of Stock Returns," explores the profitability of technical indicators, including candlestick patterns, and finds that simple trading rules, such as those based on moving averages or candlestick patterns, can occasionally outperform a random walk in certain market conditions.

However, Jorion (1997), in his work "The Risk of Speculation: The Case of Technical Analysis," warns that the reliability of candlestick patterns, including the engulfing patterns, can vary significantly across different markets and periods. Therefore, it's important to use these patterns as part of a broader trading strategy that includes other risk management techniques and technical indicators.

Application Across Markets:

This script applies to all markets (e.g., stocks, commodities, forex) and timeframes, making it a versatile tool for traders seeking to explore the statistical effectiveness of the bullish and bearish engulfing patterns in their own trading.

Conclusion:

This script allows you to backtest and visualize the effectiveness of the Bullish and Bearish Engulfing patterns across any market and timeframe. While the statistical significance of these patterns may vary, the script provides a clear framework for evaluating their performance in real-time trading conditions. Always remember to combine such patterns with other risk management strategies and indicators to enhance their predictive power.

Pivot & Source Cross StrategyPivot & ZoneCross Strategy V2

A powerful trading script combining Pivot Points, Retracement Zones, and Dynamic Stop-Loss Management. Suitable for beginners and advanced traders.

Introduction

This script enables traders to leverage Pivot Points and retracement zones for precise entry and exit points. Using price crossover detection and customizable stop-loss management, it offers a structured approach to trading various market conditions.

Features

Pivot Point Calculations: Select between Classic or Fibonacci methods for precise support and resistance levels.

Zone-Based Entry Signals: Identify price crossovers with retracement levels for optimal trade timing.

Customizable Stop-Loss Management: Automatically adjusts stop-loss levels to secure profits or limit losses.

Support for Market or Limit Orders: Choose instant market execution or specific limit entry points.

Flexible Inputs for Sources: Use Source First and Source Second to integrate external indicators like RSI and RSI MA, providing advanced customization options.

Visualization of Key Levels: Easily track retracement zones, Pivot Points, and stop-loss levels directly on the chart.

Configurable Conditions: Tailor entry/exit logic for your trading style.

How to Set Up

Choose Your Higher Timeframe (TIMEFRAME):

This determines the Pivot Points and retracement levels.

Example: Use “D” for daily pivots while trading on lower timeframes.

Select Entry Zone Patterns:

Define the pattern for detecting retracement levels:

xxx: Minor levels (steps of 10).

xx0: Intermediate levels (steps of 50).

x00: Major levels (steps of 100).

Set Entry Conditions for Long and Short Trades:

Activate or deactivate up/down conditions for xxx, xx0, or x00 patterns. Specify the count and range of crosses required for valid signals.

Configure Source Inputs (Source First and Source Second):

Assign external indicators such as RSI and RSI MA to refine entry conditions.

Tip: Adjust RSI settings in its separate indicator to suit your needs.

Select Your Order Type:

Choose between Market orders for instant execution or Limit orders for precision entries. Adjust offset zones for limit orders.

Set Up Stop-Loss Management:

Use dynamic stop-loss patterns with adjustable offsets:

HL: Stop-loss uses high/low levels of the zone.

Close: Stop-loss uses the closing price.

Customize Visualization Options:

Enable or disable xxx, xx0, x00, or 0 levels for cleaner charts. Adjust the display of retracement levels and stop-loss lines.

Apply and Monitor:

Attach the script to your chart, monitor entry/exit signals, and adjust parameters as needed.

How It Works

Calculates Pivot Points based on the chosen method ( Classic or Fibonacci ).

Detects price crossovers with retracement zones to identify potential entry points.

Dynamically adjusts stop-loss levels based on retracement zones and stop-loss patterns.

Supports both market and limit orders with customizable offsets for precise entries.

Allows integration of external sources like RSI for enhanced signal precision.

Important Notes

Use Source First and Source Second to input external indicators like RSI. You can configure RSI settings in its separate indicator to refine signals further.

Always test and optimize parameters before live trading.

Combine this script with your own analysis and proper risk management strategies.

This script is a tool to assist trading decisions but does not guarantee profits. Always trade responsibly.

MACD Aggressive Scalp SimpleComment on the Script

Purpose and Structure:

The script is a scalping strategy based on the MACD indicator combined with EMA (50) as a trend filter.

It uses the MACD histogram's crossover/crossunder of zero to trigger entries and exits, allowing the trader to capitalize on short-term momentum shifts.

The use of strategy.close ensures that positions are closed when specified conditions are met, although adjustments were made to align with Pine Script version 6.

Strengths:

Simplicity and Clarity: The logic is straightforward and focuses on essential scalping principles (momentum-based entries and exits).

Visual Indicators: The plotted MACD line, signal line, and histogram columns provide clear visual feedback for the strategy's operation.

Trend Confirmation: Incorporating the EMA(50) as a trend filter helps avoid trades that go against the prevailing trend, reducing the likelihood of false signals.

Dynamic Exit Conditions: The conditional logic for closing positions based on weakening momentum (via MACD histogram change) is a good way to protect profits or minimize losses.

Potential Improvements:

Parameter Inputs:

Make the MACD (12, 26, 9) and EMA(50) values adjustable by the user through input statements for better customization during backtesting.

Example:

pine

Copy code

macdFast = input(12, title="MACD Fast Length")

macdSlow = input(26, title="MACD Slow Length")

macdSignal = input(9, title="MACD Signal Line Length")

emaLength = input(50, title="EMA Length")

Stop Loss and Take Profit:

The strategy currently lacks explicit stop-loss or take-profit levels, which are critical in a scalping strategy to manage risk and lock in profits.

ATR-based or fixed-percentage exits could be added for better control.

Position Size and Risk Management:

While the script uses 50% of equity per trade, additional options (e.g., fixed position sizes or risk-adjusted sizes) would be beneficial for flexibility.

Avoid Overlapping Signals:

Add logic to prevent overlapping signals (e.g., opening a new position immediately after closing one on the same bar).

Backtesting Optimization:

Consider adding labels or markers (label.new or plotshape) to visualize entry and exit points on the chart for better debugging and analysis.

The inclusion of performance metrics like max drawdown, Sharpe ratio, or profit factor would help assess the strategy's robustness during backtesting.

Compatibility with Live Trading:

The strategy could be further enhanced with alert conditions using alertcondition to notify the trader of buy/sell signals in real-time.

IU Opening range Breakout StrategyIU Opening Range Breakout Strategy

This Pine Script strategy is designed to capitalize on the breakout of the opening range, which is a popular trading approach. The strategy identifies the high and low prices of the opening session and takes trades based on price crossing these levels, with built-in risk management and trade limits for intraday trading.

Key Features:

1. Risk Management:

- Risk-to-Reward Ratio (RTR):

Set a customizable risk-to-reward ratio to calculate target prices based on stop-loss levels.

Default: 2:1

- Max Trades in a Day:

Specify the maximum number of trades allowed per day to avoid overtrading.

Default: 2 trades in a day.

- End-of-Day Close:

Automatically closes all open positions at a user-defined session end time to ensure no overnight exposure.

Default: 3:15 PM

2. Opening Range Identification

- Opening Range High and Low:

The script detects the high and low of the first trading session using Pine Script's session functions.

These levels are plotted as visual guides on the chart:

- High: Lime-colored circles.

- Low: Red-colored circles.

3. Trade Entry Logic

- Long Entry:

A long trade is triggered when the price closes above the opening range high.

- Entry condition: Crossover of the price above the opening range high.

-Short Entry:

A short trade is triggered when the price closes below the opening range low.

- Entry condition: Crossunder of the price below the opening range low.

Both entries are conditional on the absence of an existing position.

4. Stop Loss and Take Profit

- Long Position:

- Stop Loss: Previous candle's low.

- Take Profit: Calculated based on the RTR.

- **Short Position:**

- **Stop Loss:** Previous candle's high.

- **Take Profit:** Calculated based on the RTR.

The strategy plots these levels for visual reference:

- Stop Loss: Red dashed lines.

- Take Profit: Green dashed lines.

5. Visual Enhancements

-Trade Level Highlighting:

The script dynamically shades the areas between the entry price and SL/TP levels:

- Red shading for the stop-loss region.

- Green shading for the take-profit region.

- Entry Price Line:

A silver-colored line marks the average entry price for active trades.

How to Use:

1.Input Configuration:

Adjust the Risk-to-Reward ratio, max trades per day, and session end time to suit your trading preferences.

2.Visual Cues:

Use the opening range high/low lines and shading to identify potential breakout opportunities.

3.Execution:

The strategy will automatically enter and exit trades based on the conditions. Review the plotted SL and TP levels to monitor the risk-reward setup.

Important Notes:

- This strategy is designed for intraday trading and works best in markets with high volatility during the opening session.

- Backtest the strategy on your preferred market and timeframe to ensure compatibility.

- Proper risk management and position sizing are essential when using this strategy in live markets.

MultiLayer Acceleration/Deceleration Strategy [Skyrexio]Overview

MultiLayer Acceleration/Deceleration Strategy leverages the combination of Acceleration/Deceleration Indicator(AC), Williams Alligator, Williams Fractals and Exponential Moving Average (EMA) to obtain the high probability long setups. Moreover, strategy uses multi trades system, adding funds to long position if it considered that current trend has likely became stronger. Acceleration/Deceleration Indicator is used for creating signals, while Alligator and Fractal are used in conjunction as an approximation of short-term trend to filter them. At the same time EMA (default EMA's period = 100) is used as high probability long-term trend filter to open long trades only if it considers current price action as an uptrend. More information in "Methodology" and "Justification of Methodology" paragraphs. The strategy opens only long trades.

Unique Features

No fixed stop-loss and take profit: Instead of fixed stop-loss level strategy utilizes technical condition obtained by Fractals and Alligator to identify when current uptrend is likely to be over (more information in "Methodology" and "Justification of Methodology" paragraphs)

Configurable Trading Periods: Users can tailor the strategy to specific market windows, adapting to different market conditions.

Multilayer trades opening system: strategy uses only 10% of capital in every trade and open up to 5 trades at the same time if script consider current trend as strong one.

Short and long term trend trade filters: strategy uses EMA as high probability long-term trend filter and Alligator and Fractal combination as a short-term one.

Methodology

The strategy opens long trade when the following price met the conditions:

1. Price closed above EMA (by default, period = 100). Crossover is not obligatory.

2. Combination of Alligator and Williams Fractals shall consider current trend as an upward (all details in "Justification of Methodology" paragraph)

3. Acceleration/Deceleration shall create one of two types of long signals (all details in "Justification of Methodology" paragraph). Buy stop order is placed one tick above the candle's high of last created long signal.

4. If price reaches the order price, long position is opened with 10% of capital.

5. If currently we have opened position and price creates and hit the order price of another one long signal, another one long position will be added to the previous with another one 10% of capital. Strategy allows to open up to 5 long trades simultaneously.

6. If combination of Alligator and Williams Fractals shall consider current trend has been changed from up to downtrend, all long trades will be closed, no matter how many trades has been opened.

Script also has additional visuals. If second long trade has been opened simultaneously the Alligator's teeth line is plotted with the green color. Also for every trade in a row from 2 to 5 the label "Buy More" is also plotted just below the teeth line. With every next simultaneously opened trade the green color of the space between teeth and price became less transparent.

Strategy settings

In the inputs window user can setup strategy setting: EMA Length (by default = 100, period of EMA, used for long-term trend filtering EMA calculation). User can choose the optimal parameters during backtesting on certain price chart.

Justification of Methodology

Let's explore the key concepts of this strategy and understand how they work together. We'll begin with the simplest: the EMA.

The Exponential Moving Average (EMA) is a type of moving average that assigns greater weight to recent price data, making it more responsive to current market changes compared to the Simple Moving Average (SMA). This tool is widely used in technical analysis to identify trends and generate buy or sell signals. The EMA is calculated as follows:

1.Calculate the Smoothing Multiplier:

Multiplier = 2 / (n + 1), Where n is the number of periods.

2. EMA Calculation

EMA = (Current Price) × Multiplier + (Previous EMA) × (1 − Multiplier)

In this strategy, the EMA acts as a long-term trend filter. For instance, long trades are considered only when the price closes above the EMA (default: 100-period). This increases the likelihood of entering trades aligned with the prevailing trend.

Next, let’s discuss the short-term trend filter, which combines the Williams Alligator and Williams Fractals. Williams Alligator

Developed by Bill Williams, the Alligator is a technical indicator that identifies trends and potential market reversals. It consists of three smoothed moving averages:

Jaw (Blue Line): The slowest of the three, based on a 13-period smoothed moving average shifted 8 bars ahead.

Teeth (Red Line): The medium-speed line, derived from an 8-period smoothed moving average shifted 5 bars forward.

Lips (Green Line): The fastest line, calculated using a 5-period smoothed moving average shifted 3 bars forward.

When the lines diverge and align in order, the "Alligator" is "awake," signaling a strong trend. When the lines overlap or intertwine, the "Alligator" is "asleep," indicating a range-bound or sideways market. This indicator helps traders determine when to enter or avoid trades.

Fractals, another tool by Bill Williams, help identify potential reversal points on a price chart. A fractal forms over at least five consecutive bars, with the middle bar showing either:

Up Fractal: Occurs when the middle bar has a higher high than the two preceding and two following bars, suggesting a potential downward reversal.

Down Fractal: Happens when the middle bar shows a lower low than the surrounding two bars, hinting at a possible upward reversal.

Traders often use fractals alongside other indicators to confirm trends or reversals, enhancing decision-making accuracy.

How do these tools work together in this strategy? Let’s consider an example of an uptrend.

When the price breaks above an up fractal, it signals a potential bullish trend. This occurs because the up fractal represents a shift in market behavior, where a temporary high was formed due to selling pressure. If the price revisits this level and breaks through, it suggests the market sentiment has turned bullish.

The breakout must occur above the Alligator’s teeth line to confirm the trend. A breakout below the teeth is considered invalid, and the downtrend might still persist. Conversely, in a downtrend, the same logic applies with down fractals.

In this strategy if the most recent up fractal breakout occurs above the Alligator's teeth and follows the last down fractal breakout below the teeth, the algorithm identifies an uptrend. Long trades can be opened during this phase if a signal aligns. If the price breaks a down fractal below the teeth line during an uptrend, the strategy assumes the uptrend has ended and closes all open long trades.

By combining the EMA as a long-term trend filter with the Alligator and fractals as short-term filters, this approach increases the likelihood of opening profitable trades while staying aligned with market dynamics.

Now let's talk about Acceleration/Deceleration signals. AC indicator is calculated using the Awesome Oscillator, so let's first of all briefly explain what is Awesome Oscillator and how it can be calculated. The Awesome Oscillator (AO), developed by Bill Williams, is a momentum indicator designed to measure market momentum by contrasting recent price movements with a longer-term historical perspective. It helps traders detect potential trend reversals and assess the strength of ongoing trends.

The formula for AO is as follows:

AO = SMA5(Median Price) − SMA34(Median Price)

where:

Median Price = (High + Low) / 2

SMA5 = 5-period Simple Moving Average of the Median Price

SMA 34 = 34-period Simple Moving Average of the Median Price

The Acceleration/Deceleration (AC) Indicator, introduced by Bill Williams, measures the rate of change in market momentum. It highlights shifts in the driving force of price movements and helps traders spot early signs of trend changes. The AC Indicator is particularly useful for identifying whether the current momentum is accelerating or decelerating, which can indicate potential reversals or continuations. For AC calculation we shall use the AO calculated above is the following formula:

AC = AO − SMA5(AO), where SMA5(AO)is the 5-period Simple Moving Average of the Awesome Oscillator

When the AC is above the zero line and rising, it suggests accelerating upward momentum.

When the AC is below the zero line and falling, it indicates accelerating downward momentum.

When the AC is below zero line and rising it suggests the decelerating the downtrend momentum. When AC is above the zero line and falling, it suggests the decelerating the uptrend momentum.

Now we can explain which AC signal types are used in this strategy. The first type of long signal is when AC value is below zero line. In this cases we need to see three rising bars on the histogram in a row after the falling one. The second type of signals occurs above the zero line. There we need only two rising AC bars in a row after the falling one to create the signal. The signal bar is the last green bar in this sequence. The strategy places the buy stop order one tick above the candle's high, which corresponds to the signal bar on AC indicator.

After that we can have the following scenarios:

Price hit the order on the next candle in this case strategy opened long with this price.

Price doesn't hit the order price, the next candle set lower high. If current AC bar is increasing buy stop order changes by the script to the high of this new bar plus one tick. This procedure repeats until price finally hit buy order or current AC bar become decreasing. In the second case buy order cancelled and strategy wait for the next AC signal.

If long trades are initiated, the strategy continues utilizing subsequent signals until the total number of trades reaches a maximum of 5. All open trades are closed when the trend shifts to a downtrend, as determined by the combination of the Alligator and Fractals described earlier.

Why we use AC signals? If currently strategy algorithm considers the high probability of the short-term uptrend with the Alligator and Fractals combination pointed out above and the long-term trend is also suggested by the EMA filter as bullish. Rising AC bars after period of falling AC bars indicates the high probability of local pull back end and there is a high chance to open long trade in the direction of the most likely main uptrend. The numbers of rising bars are different for the different AC values (below or above zero line). This is needed because if AC below zero line the local downtrend is likely to be stronger and needs more rising bars to confirm that it has been changed than if AC is above zero.

Why strategy use only 10% per signal? Sometimes we can see the false signals which appears on sideways. Not risking that much script use only 10% per signal. If the first long trade has been open and price continue going up and our trend approximation by Alligator and Fractals is uptrend, strategy add another one 10% of capital to every next AC signal while number of active trades no more than 5. This capital allocation allows to take part in long trades when current uptrend is likely to be strong and use only 10% of capital when there is a high probability of sideways.

Backtest Results

Operating window: Date range of backtests is 2023.01.01 - 2024.11.01. It is chosen to let the strategy to close all opened positions.

Commission and Slippage: Includes a standard Binance commission of 0.1% and accounts for possible slippage over 5 ticks.

Initial capital: 10000 USDT

Percent of capital used in every trade: 10%

Maximum Single Position Loss: -5.15%

Maximum Single Profit: +24.57%

Net Profit: +2108.85 USDT (+21.09%)

Total Trades: 111 (36.94% win rate)

Profit Factor: 2.391

Maximum Accumulated Loss: 367.61 USDT (-2.97%)

Average Profit per Trade: 19.00 USDT (+1.78%)

Average Trade Duration: 75 hours

How to Use

Add the script to favorites for easy access.

Apply to the desired timeframe and chart (optimal performance observed on 3h BTC/USDT).

Configure settings using the dropdown choice list in the built-in menu.

Set up alerts to automate strategy positions through web hook with the text: {{strategy.order.alert_message}}

Disclaimer:

Educational and informational tool reflecting Skyrex commitment to informed trading. Past performance does not guarantee future results. Test strategies in a simulated environment before live implementation

These results are obtained with realistic parameters representing trading conditions observed at major exchanges such as Binance and with realistic trading portfolio usage parameters.

Liquid Pours XtremeStrategy Description: Liquid Pours Xtreme

The Liquid Pours Xtreme is an innovative trading strategy that combines the analysis of specific time-based patterns with price comparisons to identify potential opportunities in the forex market. Designed for traders seeking a structured methodology based on clear rules, this strategy offers integration with Telegram for real-time alerts and provides visual tools to enhance trade management.

Key Features:

Analysis of Specific Time Patterns: The strategy captures and compares closing prices at two key moments during the trading day, identifying recurring patterns that may indicate future market movements.

Dynamic SL and TP Levels Implementation: Utilizes tick-based calculations to set Stop-Loss and Take-Profit levels, adapting to the current market volatility.

Advanced Telegram Integration: Provides detailed alerts including information such as the asset, signal time, entry price, and SL/TP levels, facilitating real-time decision-making.

Complete Customization: Allows users to adjust key parameters, including operation schedules, weekdays, and visual settings, adapting to different trading styles.

Enhanced Chart Visualization: Includes visual elements like candle color changes based on signal state, event markers, and halos to highlight important moments.

Default Strategy Properties: Specific configuration for optimal risk management and simulation.

How the Strategy Works

Capturing Prices at Key Moments:

- The strategy records the closing price at two user-defined specific times. These times typically correspond to periods of high market volatility, such as the opening of the European session and the US pre-market.

- Rationale: Volatility and trading volume usually increase during these times, presenting opportunities for significant price movements.

Generating Signals Based on Price Comparison:

- Buy Signal: If the second closing price is lower than the first, it indicates possible accumulation and is interpreted as a bullish signal.

- Sell Signal: If the second closing price is higher than the first, it suggests possible distribution and is interpreted as a bearish signal.

- Signals are only generated on selected trading days, allowing you to avoid days with lower liquidity or higher risk.

Calculating Dynamic SL and TP Levels:

- Stop-Loss (SL) and Take-Profit (TP) levels are calculated based on the entry price and a user-defined number of ticks, adapting to market volatility.

- The strategy offers the option to base these levels on the close of the signal candle or the open of the next candle, providing flexibility according to the trader's preference.

- SL and TP boxes are drawn on the chart for visual reference, facilitating trade management.

Automatic Execution and Alerts:

- Upon signal generation, the strategy automatically executes a market order (buy or sell).

- Sends a detailed alert to your Telegram channel, including essential information for quick decision-making.

Visual Elements:

- Colors candles based on the signal state: buy, sell, or neutral, allowing for quick trend identification.

- Provides a smooth color transition between signal states and uses markers and halos to highlight important events and signals on the chart.

Trade Management:

- Manages open trades with automatic exit conditions based on the established SL and TP levels.

- Includes mechanisms to prevent exceeding TradingView's limitations on boxes and labels, ensuring optimal script performance.

Originality and utility:

- This strategy incorporates a unique approach focusing on specific time patterns and their relationship to institutional activity in the market.

How to Use the Strategy

Add the Script to the Chart:

- Go to the indicators menu in TradingView.

- Search for " Liquid Pours Xtreme " and add it to your chart.

Set Up Telegram Alerts:

- Enter your Telegram Chat ID in the script parameters to receive alerts.

- Customize the Buy and Sell alert messages as desired.

Configure Time Patterns:

- Set the hours and minutes for the two times you want to compare closing prices, aligning them with relevant market sessions or events.

Set SL and TP Parameters:

- Define the number of ticks for the Stop-Loss and Take-Profit levels, adapting them to the asset you're trading and your risk tolerance.

- Choose the basis for SL and TP calculation (close of the signal candle or open of the next candle).

Select Trading Days:

- Enable or disable trading on specific days of the week, allowing you to avoid days with lower activity or unexpected volatility.

Customize Visual Elements:

- Adjust the colors and styles of visual elements to enhance readability and suit your personal preferences.

Monitor the Strategy:

- Observe the chart for signals and use Telegram alerts to stay informed of new opportunities, even when you're not at your terminal.

Testing and Optimization:

- Use TradingView's backtesting features to evaluate the historical performance of the strategy with different parameters.

- Adjust and optimize the parameters based on the results and your own analysis.

Adjust the Strategy Properties:

- Ensure that the strategy properties (order size, commission, slippage) are aligned with your trading account and platform to obtain realistic results.

Strategy Properties (Important)

This script backtest is conducted on M30 EURUSD , using the following backtesting properties:

Initial Capital: $10,000

Order Size: 50,000 Contracts (equivalent to 0.5% of the capital)

Commission: $0.20 per order

Slippage: 1 tick

Pyramiding: 1 order

Verify Price for Limit Orders: 0 ticks

Recalculate on Order Execution: Enabled

Recalculate on Every Tick: Enabled

Recalculate After Order Filled: Enabled

Bar Magnifier for Backtesting Precision: Enabled

We use these properties to ensure a realistic preview of the backtesting system. Note that default properties may vary for different reasons:

- Order Size: It is essential to calculate the contract size according to the traded asset and desired risk level.

- Commission and Slippage: These costs can vary depending on the market and instrument; there is no default value that might return realistic results.

We strongly recommend all users adjust the Properties within the script settings to align with their accounts and trading platforms to ensure the results from the strategies are realistic.

Backtesting Results:

- Net Profit: $4,037.50 (40.37%)

- Total Closed Trades : 292

- Profitability Percentage: 26.71%

- Profit Factor: 1.369

- Max Drawdown: $769.30 (6.28%)

- Average Trade: $13.83 (0.03%)

- Average Bars in Trades: 11

These results were obtained under the mentioned conditions and properties, providing an overview of the strategy's historical performance.

Interpreting Results:

- The strategy has demonstrated profitability in the analyzed period, although with a win rate of 26.71%, indicating that success relies on a favorable risk-reward ratio.

- The profit factor of 1.369 suggests that total gains exceed total losses by that proportion.

- It is crucial to consider the maximum drawdown of 6.28% when evaluating the strategy's suitability to your risk tolerance.

Risk Warning:

Trading leveraged financial instruments carries a high level of risk and may not be suitable for all investors. Before deciding to trade, you should carefully consider your investment objectives, level of experience, and risk tolerance. Past performance does not guarantee future results. It is essential to conduct additional testing and adjust the strategy according to your needs.

---

What Makes This Strategy Original?

Time-Based Pattern Approach: Unlike conventional strategies, this strategy focuses on identifying time patterns that reflect institutional activity and macroeconomic events that can influence the market.

Advanced Technological Integration: The combination of automatic execution and customized alerts via Telegram provides an efficient and modern tool for active traders.

Customization and Adaptability: The wide range of adjustable parameters allows the strategy to be tailored to different assets, time zones, and trading styles.

Enhanced Visual Tools: Incorporated visual elements facilitate quick market interpretation and informed decision-making.

Additional Considerations

Continuous Testing and Optimization: Users are encouraged to perform additional backtesting and optimize parameters according to their own observations and requirements.

Complementary Analysis: Use this strategy in conjunction with other indicators and fundamental analysis to reinforce decision-making.

Rigorous Risk Management: Ensure that SL and TP levels, as well as position sizing, align with your risk management plan.

Updates and Support: I am committed to providing updates and improvements based on community feedback. For inquiries or suggestions, feel free to contact me.

---

Example Configuration

Assuming you want to use the strategy with the following parameters:

Telegram Chat ID: Your unique Telegram Chat ID

First Time (Hour:Minute): 6:30

Second Time (Hour:Minute): 7:30

SL Ticks: 100

TP Ticks: 400

SL and TP Basis: Close of the Signal Candle

Trading Days: Tuesday, Wednesday, Thursday

Simulated Initial Capital: $10,000

Risk per Trade in Simulation: $50 (-0.5% of capital)

Slippage and Commissions in Simulation: 1 tick of slippage and $0.20 commission per trade

---

Conclusion

The Liquid Pours Xtreme strategy offers an innovative approach by combining specific time analysis with robust risk management and modern technological tools. Its original and adaptable design makes it valuable for traders looking to diversify their methods and capitalize on opportunities based on less conventional patterns.

Ready for immediate implementation in TradingView, this strategy can enrich your trading arsenal and contribute to a more informed and structured approach to your operations.

---

Final Disclaimer:

Financial markets are volatile and can present significant risks. This strategy should be used as part of a comprehensive trading approach and does not guarantee positive results. It is always advisable to consult with a professional financial advisor before making investment decisions.

---

MultiLayer Awesome Oscillator Saucer Strategy [Skyrexio]Overview

MultiLayer Awesome Oscillator Saucer Strategy leverages the combination of Awesome Oscillator (AO), Williams Alligator, Williams Fractals and Exponential Moving Average (EMA) to obtain the high probability long setups. Moreover, strategy uses multi trades system, adding funds to long position if it considered that current trend has likely became stronger. Awesome Oscillator is used for creating signals, while Alligator and Fractal are used in conjunction as an approximation of short-term trend to filter them. At the same time EMA (default EMA's period = 100) is used as high probability long-term trend filter to open long trades only if it considers current price action as an uptrend. More information in "Methodology" and "Justification of Methodology" paragraphs. The strategy opens only long trades.

Unique Features

No fixed stop-loss and take profit: Instead of fixed stop-loss level strategy utilizes technical condition obtained by Fractals and Alligator to identify when current uptrend is likely to be over (more information in "Methodology" and "Justification of Methodology" paragraphs)

Configurable Trading Periods: Users can tailor the strategy to specific market windows, adapting to different market conditions.

Multilayer trades opening system: strategy uses only 10% of capital in every trade and open up to 5 trades at the same time if script consider current trend as strong one.

Short and long term trend trade filters: strategy uses EMA as high probability long-term trend filter and Alligator and Fractal combination as a short-term one.

Methodology

The strategy opens long trade when the following price met the conditions:

1. Price closed above EMA (by default, period = 100). Crossover is not obligatory.

2. Combination of Alligator and Williams Fractals shall consider current trend as an upward (all details in "Justification of Methodology" paragraph)

3. Awesome Oscillator shall create the "Saucer" long signal (all details in "Justification of Methodology" paragraph). Buy stop order is placed one tick above the candle's high of last created "Saucer signal".

4. If price reaches the order price, long position is opened with 10% of capital.

5. If currently we have opened position and price creates and hit the order price of another one "Saucer" signal another one long position will be added to the previous with another one 10% of capital. Strategy allows to open up to 5 long trades simultaneously.

6. If combination of Alligator and Williams Fractals shall consider current trend has been changed from up to downtrend, all long trades will be closed, no matter how many trades has been opened.

Script also has additional visuals. If second long trade has been opened simultaneously the Alligator's teeth line is plotted with the green color. Also for every trade in a row from 2 to 5 the label "Buy More" is also plotted just below the teeth line. With every next simultaneously opened trade the green color of the space between teeth and price became less transparent.

Strategy settings

In the inputs window user can setup strategy setting: EMA Length (by default = 100, period of EMA, used for long-term trend filtering EMA calculation). User can choose the optimal parameters during backtesting on certain price chart.

Justification of Methodology

Let's go through all concepts used in this strategy to understand how they works together. Let's start from the easies one, the EMA. Let's briefly explain what is EMA. The Exponential Moving Average (EMA) is a type of moving average that gives more weight to recent prices, making it more responsive to current price changes compared to the Simple Moving Average (SMA). It is commonly used in technical analysis to identify trends and generate buy or sell signals. It can be calculated with the following steps:

1.Calculate the Smoothing Multiplier:

Multiplier = 2 / (n + 1), Where n is the number of periods.

2. EMA Calculation

EMA = (Current Price) × Multiplier + (Previous EMA) × (1 − Multiplier)

In this strategy uses EMA an initial long term trend filter. It allows to open long trades only if price close above EMA (by default 50 period). It increases the probability of taking long trades only in the direction of the trend.

Let's go to the next, short-term trend filter which consists of Alligator and Fractals. Let's briefly explain what do these indicators means. The Williams Alligator, developed by Bill Williams, is a technical indicator designed to spot trends and potential market reversals. It uses three smoothed moving averages, referred to as the jaw, teeth, and lips:

Jaw (Blue Line): The slowest of the three, based on a 13-period smoothed moving average shifted 8 bars ahead.

Teeth (Red Line): The medium-speed line, derived from an 8-period smoothed moving average shifted 5 bars forward.

Lips (Green Line): The fastest line, calculated using a 5-period smoothed moving average shifted 3 bars forward.

When these lines diverge and are properly aligned, the "alligator" is considered "awake," signaling a strong trend. Conversely, when the lines overlap or intertwine, the "alligator" is "asleep," indicating a range-bound or sideways market. This indicator assists traders in identifying when to act on or avoid trades.

The Williams Fractals, another tool introduced by Bill Williams, are used to pinpoint potential reversal points on a price chart. A fractal forms when there are at least five consecutive bars, with the middle bar displaying the highest high (for an up fractal) or the lowest low (for a down fractal), relative to the two bars on either side.

Key Points:

Up Fractal: Occurs when the middle bar has a higher high than the two preceding and two following bars, suggesting a potential downward reversal.